Charter Communications - the inverse SpaceX trade?

Uncertainty around competition from new technologies and a heavy debt burden have pushed Charter's share price to its lowest level in a decade, creating the opportunity for substantial upside from a recovery.

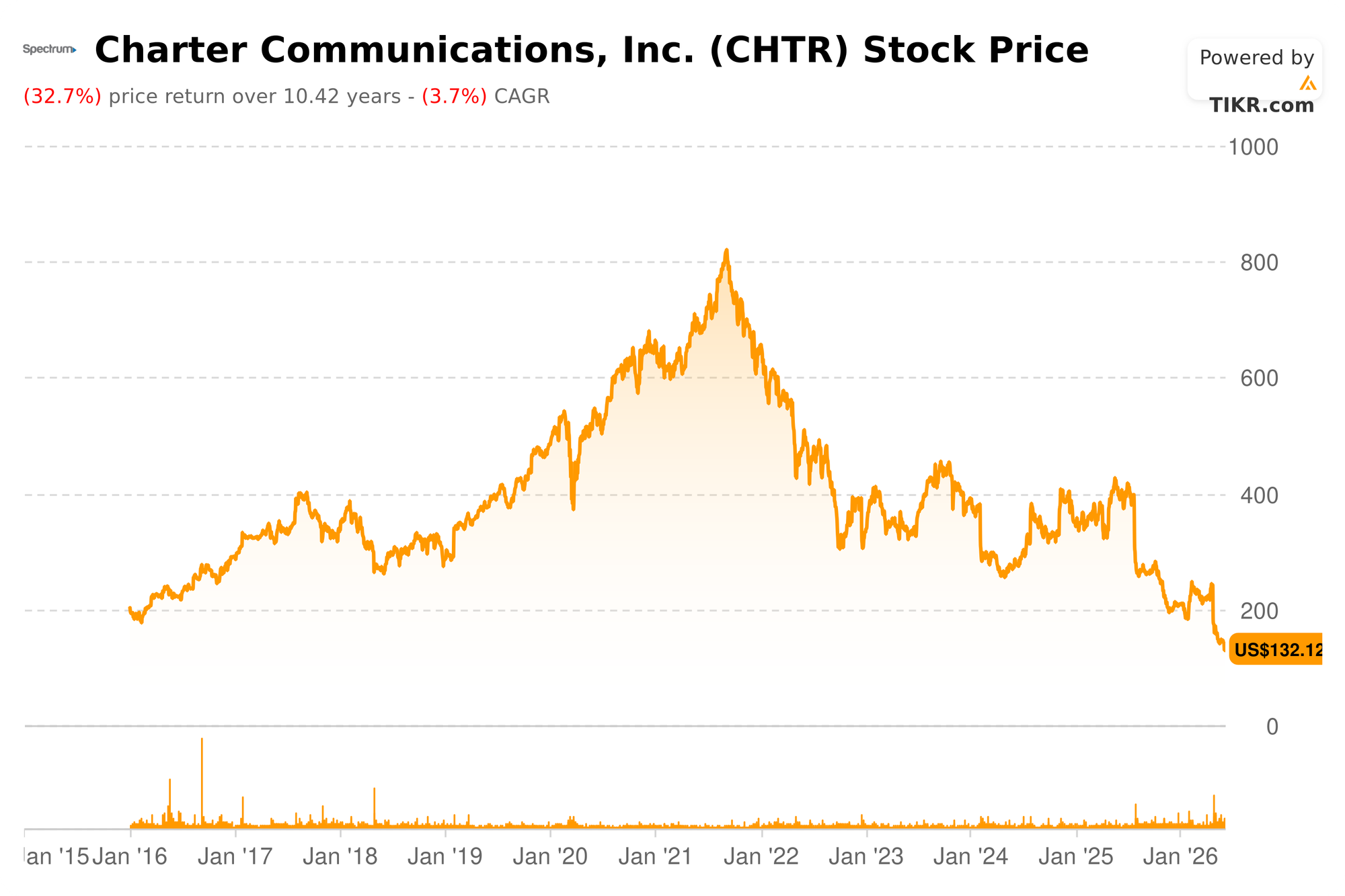

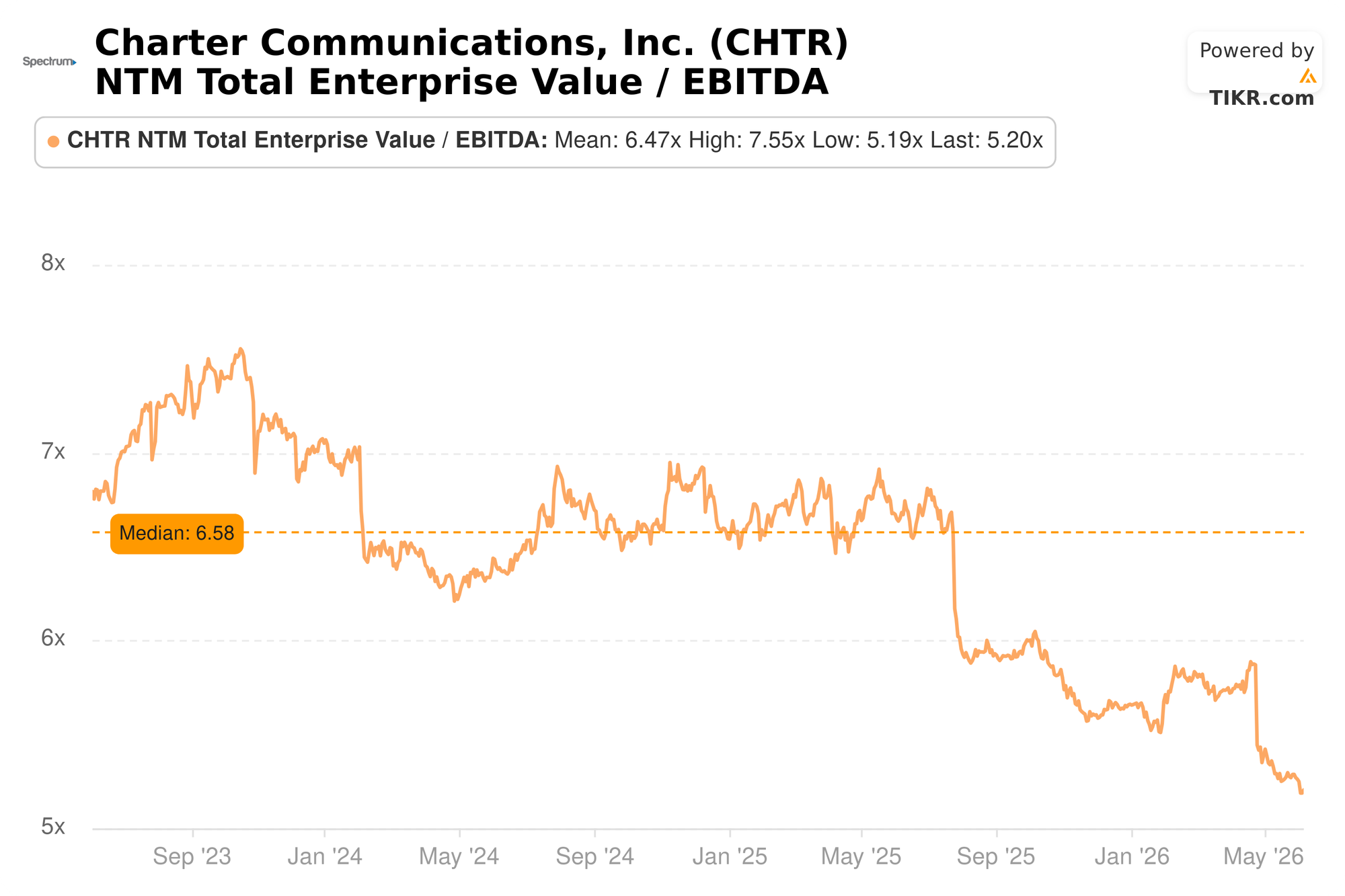

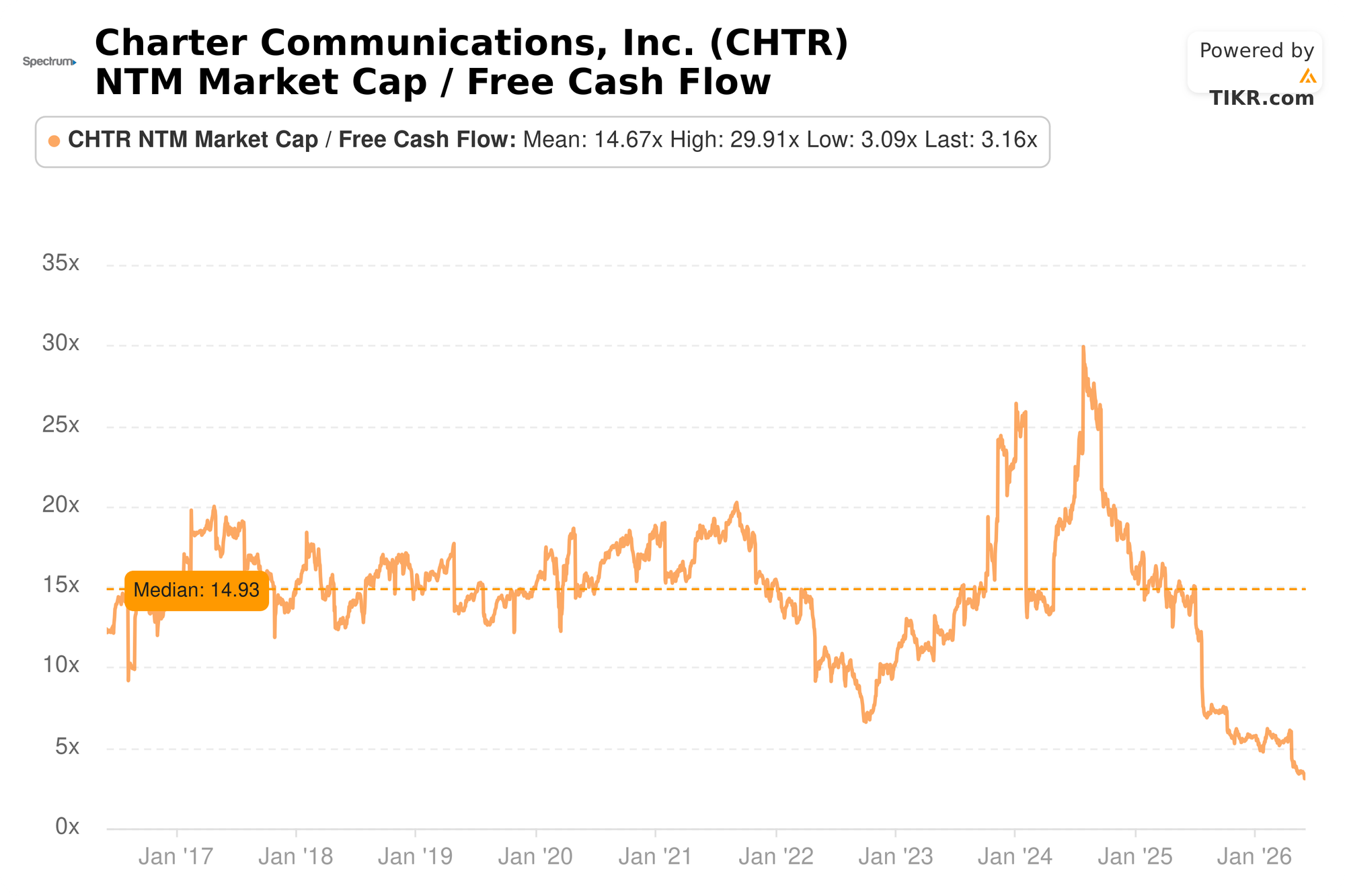

In this time of market euphoria, I thought I'd bring you a short write-up on a company that's been all but left for dead. Charter Communications (CHTR) trades at not just a 52 week low, but a decade low. Its forward valuation multiple for several metrics including P/FCF (3.20x) and EV/EBITDA (5.2x) is also at the lowest level in the last 10 years. As you can see from the price chart below, there have been some rather dramatic sentiment/narrative shifts over this 10-year period.

Business overview

In 2016, Charter underwent a transformative merger with Time Warner Cable alongside acquiring Bright House Networks; two deals that propelled the company to become the second largest (coaxial)cable operator in the US behind Comcast. The cable business was originally built around cable television, but with the advent of the internet and a shift in consumer preference towards streaming, the business model has increasingly moved towards the provision of high-speed internet.

Around 15 years ago, fibre over-builders entered the market for high-speed internet as direct competitors to the legacy cable companies. These fibre optic networks are purpose-built for the kind of symmetrical gigabit traffic demanded by modern internet users and substantial investment has been required by the legacy cable companies to adapt their networks to match this capability - having originally been designed for one-way TV traffic. Charter is in the middle of this upgrade process, and expects to be able to provide multi-gig download and 1Gbps upload across 50% of its network by the end of 2026, with the other 50% being completed in 2027.

In 2018, Charter launched Spectrum Mobile, becoming a Mobile Virtual Network Operator (MVNO) using Verizon's network. The company has been able to substantially reduce its dependency on Verizon by offloading wireless traffic to its own cable network using WiFi from home routers and public hotspots, and CBRS (Citizens Broadband Radio Service) antennas positioned in dense urban areas. Today, around 88% of all wireless traffic from Spectrum Mobile customers is handled by Charter directly, allowing it to compete effectively with full-fat Mobile Network Operators (MNOs) that have their own spectrum licences (e.g. T-Mobile, AT&T and Verizon).

While Charter has been making inroads into mobile, the MNOs have been encroaching on Charter's residential internet by offering fixed-wireless internet packages to their mobile customers. Fixed-wireless is generally an inferior product, with lower bandwidth and higher latency than cable or fibre, but it's often offered at a lower price-point making it attractive to a certain subset of customers.

The other new entrant to the internet market is LEO satellite provided by Starlink (SpaceX). Rapid global adoption of Starlink internet has been a primary driver of the hype around the SpaceX IPO, but so far its usefulness has been largely limited to sparsely populated rural areas. This could change if they're able to achieve their ambitions of launching a new constellation of v3 satellites with 10x the downlink and 24x the uplink of their current v2 satellites. These v3 satellites are much larger (and heavier) than the v2 and can't be carried by the falcon-9 rocket, which has been used for all the launches so far. Deploying the v3 constellation will therefore require the new, larger capacity, starship rocket Spacex is currently developing.

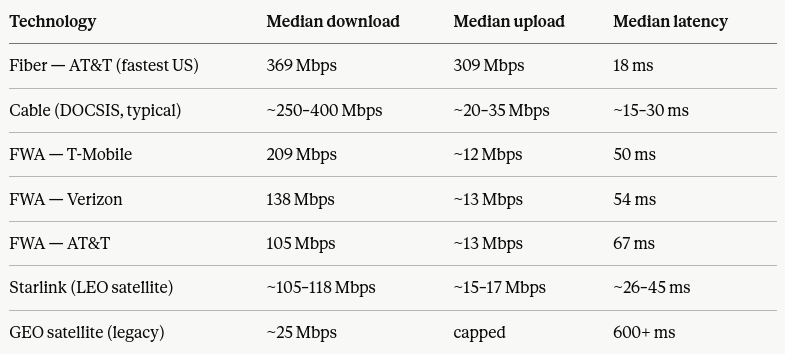

The table below shows some median download, upload and latency figures for each technology from Ookla research. Don't take these as gospel, as they were collected from a few different sources and date back to 2025, but they give you a general picture.

As you can see, cable is competitive with fibre on download speeds and latency, but currently lags on upload speed, as we've discussed. All other technologies perform worse across the board.

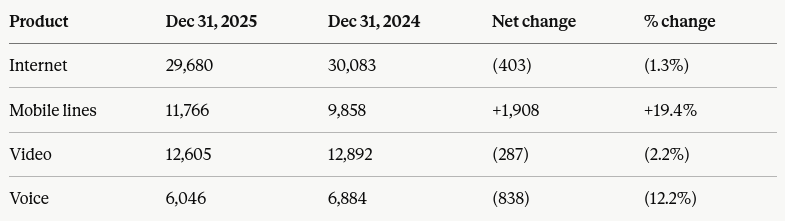

So how have these forces impacted Charter? From the table below, you can see the company had a net 1.3% (403k) decrease in internet customers during 2025 while mobile lines increased by 19.4% (1,908k). The structural decline of video and voice is also clearly visible with 2.2% (287k) and 12.2% (838k) decreases, respectively.

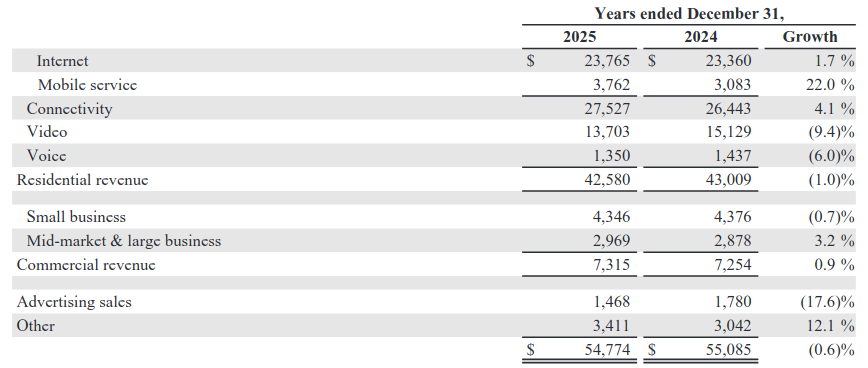

The revenue picture is a little brighter in some areas, with product mix changes leading to growth in internet revenue despite the customer number declining. Video on the other hand saw an even greater revenue fall as product mix and pricing changes compounded the drop in customers. Overall revenue decreased by a modest 0.6%.

Another factor that has contributed to Charter's fall from grace is its heavy debt burden. In the years of near-zero interest rates, being highly leveraged was seen as attractive for equity holders, as it juiced returns. Post-2022, when inflation forced up interest rates globally, this is no longer the case, and Charter's 4.23x net debt to EBITDA is unpalatable for investors.

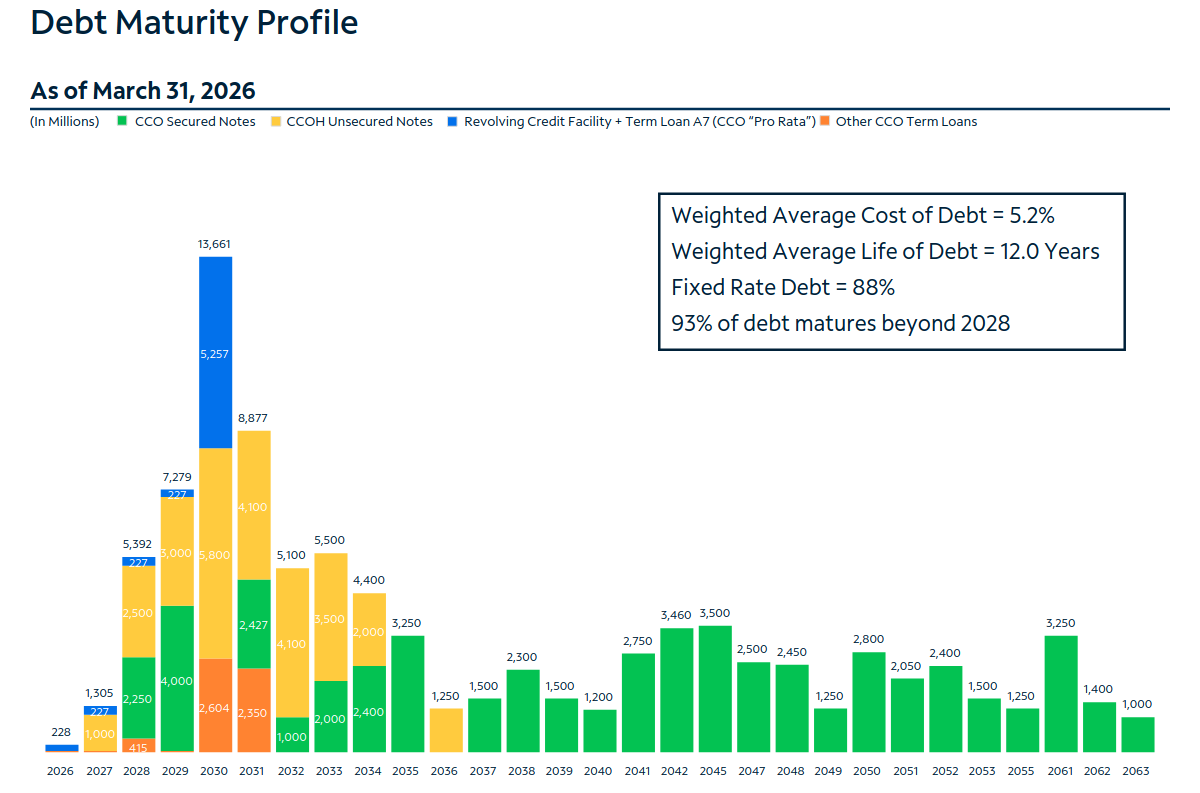

Looking at the company's current debt maturity profile, we see a relatively healthy picture: the debt has a weighted average cost of 5.2%, weighted average life of 12.0 years and is 88% fixed rate. That said, you can see a wall of maturities starting around 2028 and peaking in 2030 that will need to be refinanced or repaid in the medium-term.

The long tail of maturities can be framed as an asset since most of this debt has a low fixed cost and currently trades for a fraction of its face value. This creates opportunities for Charter to realise significant gains on extinguishment, were they to start repurchasing and retiring the longer-dated bonds.

Cox Communications merger

At this point, I think it's appropriate to mention the Cox Communications merger currently in progress. In May 2025, Charter announced it would combine with Cox Communications in a deal valuing Cox at $34.5bn ($21.9bn for the equity + $12.6bn for the debt). Cox shareholders will receive the following consideration:

- $4bn in cash;

- $6bn in convertible preferred units paying a 6.875% coupon;

- and 33.5m common partnership units, exchangeable for Charter common shares valued at $11.9bn using the CHTR share price at the time of c$354.

The total valuation for Cox (including the debt assumed) is 6.44x its 2025 estimated adjusted EBITDA of $5.3-5.4bn, matching the EV/EBITDA multiple of Charter at that time.

One crucial point of note is the use of a fixed number of common partnership units as consideration rather than a fixed monetary value. This means Charter shareholders aren't going to be further diluted as a result of the fall in the share price since announcement.

As you've probably noted already, Cox has significantly lower leverage than Charter. Merging with Cox will consequently bring down Charter's leverage to 3.9x without any further action. That said, Charter is aiming to further reduce leverage to the lower end of 3.5-3.75x within 3 years of the deal closing.

The transaction has already received regulatory approval from the FCC and all the required states except California, with which negotiations are still underway. If it's going to close, it really needs to happen before the 15th September 2026, when clearance from the DOJ expires. So there is some time pressure that's likely to draw out concessions from the company.

Valuation and investment outlook

Share price: $133.34

Market capitalisation: $16,203m

Enterprise value: $117,193m

I've given you an overview of the company and the pressures it's facing; now let me present the opportunity. In FY25, Charter generated a net profit of $4,987m and $4,418m in free cash flow. As I've discussed above, the company has been investing heavily in upgrading its network, but that capital expenditure is tailing off over the next couple of years, and should result in an upward FCF inflection from around 2027 onwards.

At time of writing, the market is currently valuing the whole company at $16,203m, or 3.26x lasts year's earnings and 3.68x last year's free cash flow. The forward multiples, based on analyst consensus earnings and FCF, are 2.97x and 3.20x, respectively. As I said at the top, the company is the cheapest it's been for more than a decade.

Looking at EV/EBITDA for the last 3 years (so it excludes the prior zero-rate period), we can see the median multiple has been 6.58x; broadly in line with peers and significantly above the current 5.2x at which Charter trades today.

On a FCF basis, the median multiple for the last decade has been 14.93x versus the company's 3.16x today.

The crux of the problem is the market's aversion to Charter's leverage: it's peers are all around 3x levered and trade at 6-9x earnings/FCF - arguably still an attractive level and towards the lower end of their historic range. As Charter's leverage starts to fall back in line with its peers, we should expect to see its earnings/FCF multiple expand, providing the impetus for a potential 2-3x rise in the share price. This doesn't account for any upward inflection in FCF, which would provide further upside.

We also haven't discussed share repurchases. Charter spent $5,132m on share repurchases during FY25, and plans to continue returning excess FCF to shareholders in this manner going forwards. At the current share price, it could repurchase ~30% of its shares each year, which would dramatically boost returns if sustained over a multi-year period.

In summary, Charter has been left for dead due to a combination of high leverage and fears around competition from emerging technologies, not least Starlink's LEO satellites. If you believe neither of these factors will prove existential to Charter's business, the current share price is highly attractive and offers very substantial upside over a 3-5 year time horizon.